Financial Stability Implications of Private Credit Growth

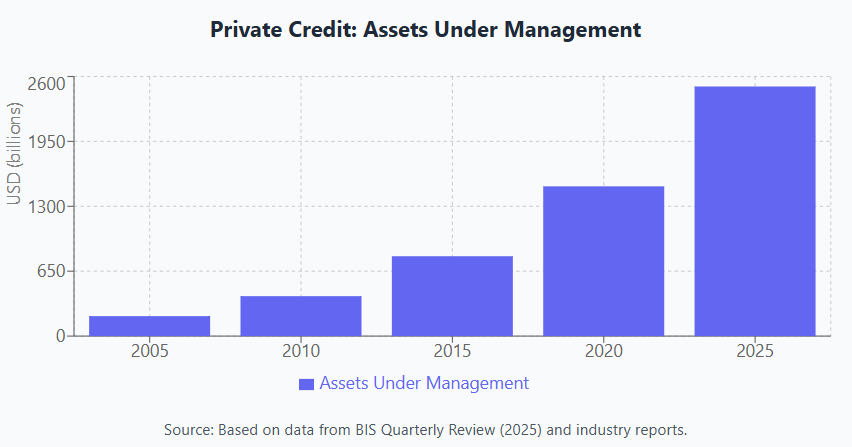

The rapid expansion of private credit markets represents one of the most significant transformations in global finance since the 2008 crisis. As this sector approaches $2.5 trillion in assets under management, questions about its implications for financial stability have become increasingly urgent. This blog examines the complex relationship between private credit growth and systemic risk, exploring how structural differences between banks and non-bank lenders—including maturity profiles, regulatory frameworks, and portfolio concentration—might influence market behaviour during economic stress. Drawing on recent research, we analyse how private credit's distinctive "maturity wall" functions as both a commitment device that enhances borrower discipline and a potential source of inefficient liquidation during downturns. By exploring these dynamics, we provide insights into whether private credit represents a diversification of financial risk or a migration of vulnerabilities to less regulated corners of the financial system. As private credit continues its remarkable growth trajectory, understanding these mechanisms becomes essential for investors, regulators, and policymakers seeking to balance innovation with stability in the evolving lending landscape.

Phoenicia Research Centre

5/2/20258 min read

The Quiet Revolution in Corporate Lending

Since the 2008 global financial crisis, one of the most profound shifts in financial markets has been the extraordinary rise of private credit. Once a niche corner of alternative investments, private credit funds now manage approximately $2.5 trillion globally and have expanded into increasingly diverse sectors, from traditional corporate lending to infrastructure, technology, and sustainable finance.

This growth has been driven by a perfect storm of factors: regulatory constraints on traditional banks, institutional investors' search for yield in a low-interest rate environment, and borrowers seeking more flexible financing options. Yet despite its increasing importance in the global financial ecosystem, our understanding of private credit's implications for financial stability remains incomplete.

Unlike banks, which can extend loan maturities during periods of stress, private credit funds—particularly those structured as closed-end vehicles—operate with a "maturity wall" that limits their ability to roll over debt. This structural feature creates fundamentally different incentives for both lenders and borrowers, with potentially significant consequences for financial stability.

In this blog, we'll explore these dynamics in depth, examining how private credit's unique characteristics might influence market behaviour during periods of economic stress and what this means for systemic risk.

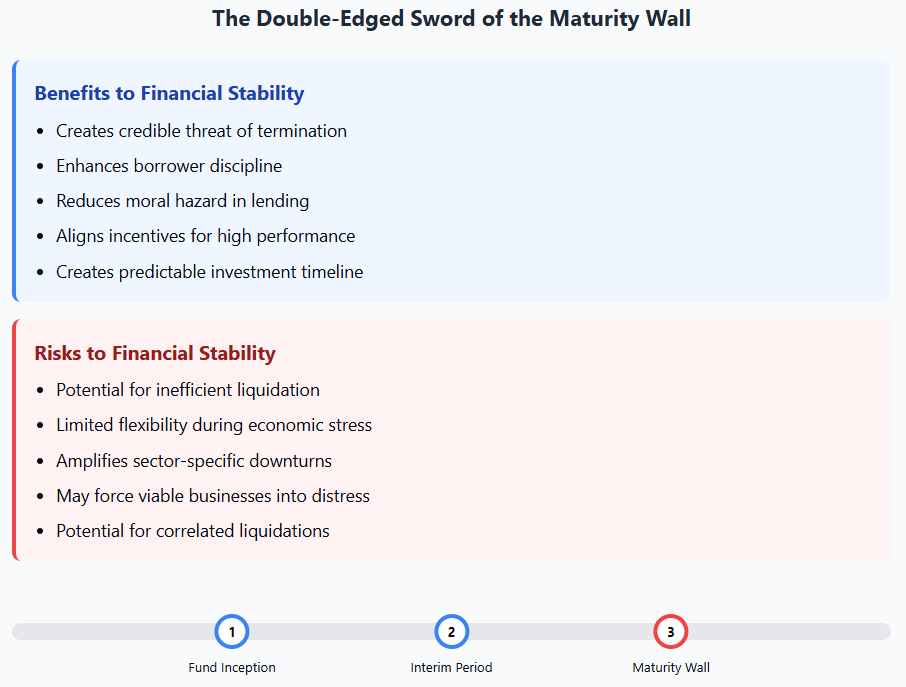

The Maturity Wall: Double-Edged Sword for Financial Stability

At the heart of private credit's structural difference from traditional bank lending is the concept of the "maturity wall"—the fixed lifetime of many private credit funds that constrains their ability to extend loan maturities indefinitely.

The Commitment Device: Enhancing Discipline Through Structure

The maturity wall serves an important economic function that may actually enhance financial stability in certain ways. Research by Albuquerque and Zawadowski (2025) demonstrates that because private credit funds cannot commit to rolling over loans beyond their maturity date, this creates a credible threat of termination that incentivizes borrowers to exert greater effort in managing their businesses.

This "commitment device" helps address a fundamental agency problem in corporate lending. When borrowers know that lenders can indefinitely extend loan maturities—as banks often do—this can reduce their incentives to perform at the highest level. In contrast, private credit's structural limitation creates what Bolton and Scharfstein (1990) describe as "an ex-ante incentive for the borrower to work hard leading up to the interim period".

The evidence suggests this mechanism is working. In a study comparing loans provided by private credit funds and banks, Jang (2024) found that direct lenders are more likely to renegotiate loans during a fund's lifetime, but typically only when private equity sponsors inject additional equity. This reinforces the disciplining effect that private credit's structure creates.

The Risk of Inefficient Liquidation

However, the same structural feature that enhances borrower discipline also creates risks during economic downturns. When private credit funds reach their maturity date, they may be forced to liquidate investments even when it would be more efficient to extend loan maturities. This can lead to a situation where perfectly viable businesses face unnecessary financial distress simply because their lenders lack the flexibility to extend financing.

As Albuquerque and Zawadowski note, "In contrast to private credit, banks' longer horizon allows for renegotiation and extension of non-performing bank loans." The inability to renegotiate private credit loans beyond their maturity generates incentives to exert effort at the cost of "excessive liquidation when projects fail in the interim period".

This risk of inefficient liquidation could become particularly problematic during economic downturns when many borrowers simultaneously face financial stress.

Comparative Behaviour During Economic Stress

One of the most important questions for financial stability is how private credit lenders behave during periods of economic stress compared to banks. Here, the evidence presents a mixed picture.

Different Reactions to Economic Downturns

Research suggests that bank credit is more sensitive to economic downturns than non-bank credit. Boyarchenko and Elias (2024) found that expansions in non-bank credit have a shorter-lived negative predictive relationship with future average real GDP growth than expansions in bank credit.

Intriguingly, non-bank credit expansions predict a lower probability of extreme negative growth realisations 3-4 years into the future, while bank credit expansions predict a higher crisis probability at the same horizons. This suggests that "credit booms financed by non-banks appear to have a less pernicious effect on future real outcomes".

This difference in crisis predictability may stem from several factors, including:

Private credit funds' greater willingness to lend to riskier borrowers but with more stringent covenant structures

The absence of deposit-funding and associated run risks

The extended timeframe of closed-end funds that reduces pressure for short-term performance

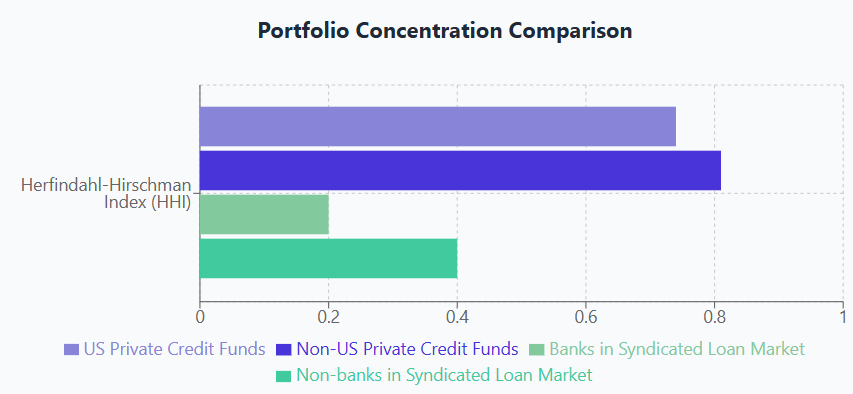

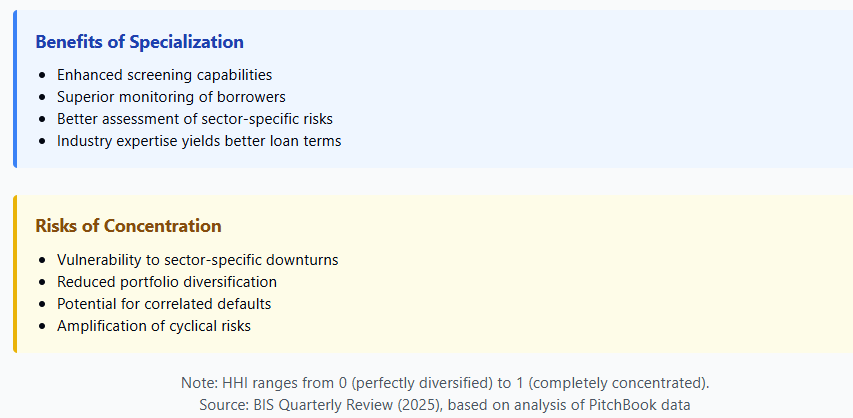

Portfolio Concentration: Specialisation vs. Diversification

Despite private credit's growth across industries, individual funds maintain highly concentrated portfolios. According to data from PitchBook analyzed by the BIS, the Herfindahl-Hirschman Index (HHI), a measure of portfolio concentration, averages 0.74 for US-based funds and 0.81 for non-US funds. This is significantly higher than the concentration levels in bank lending.

Such concentration yields benefits through specialisation, which improves screening and monitoring capabilities. However, it also creates vulnerability to sector-specific downturns.

The tension between specialisation and diversification raises important financial stability questions: While specialised lenders may better understand and price risk in their chosen sectors, their concentrated exposure could lead to amplified losses during sector-specific downturns. This represents a different risk profile than more diversified bank lenders.

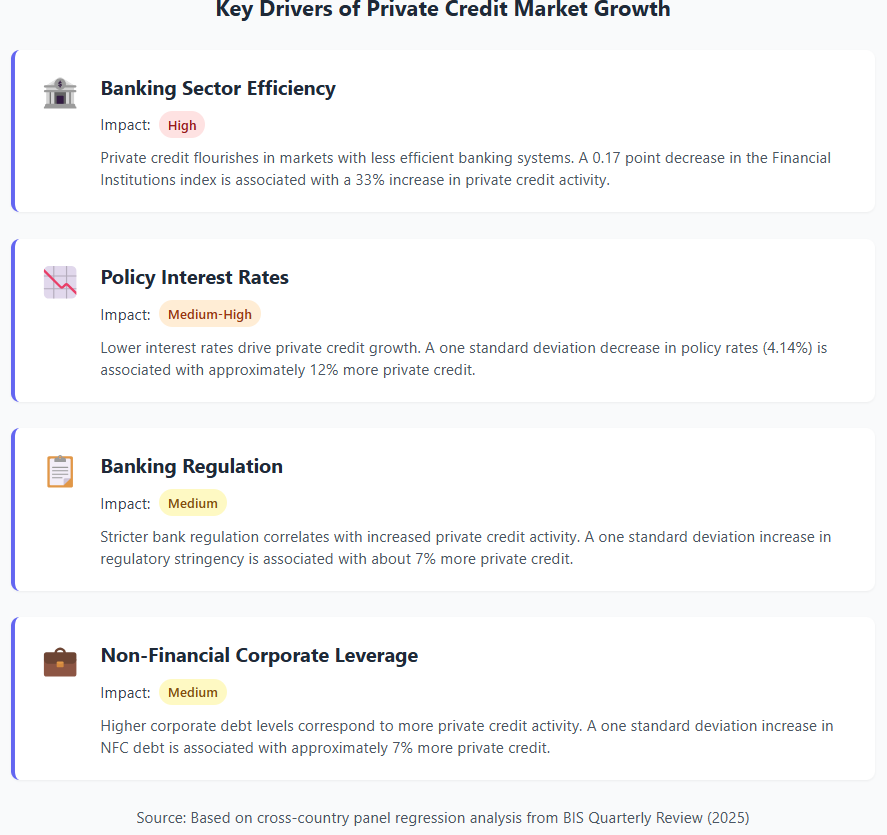

The Drivers of Private Credit Growth and Their Stability Implications

Understanding what drives private credit's growth helps illuminate its potential financial stability implications.

Cross-country evidence from the BIS shows that private credit's footprint is larger in countries with lower policy rates, more stringent banking regulation, and a less efficient banking sector. In a panel covering 45 countries between 2010 and 2019, all three variables have a statistically significant impact on loan originations by private credit funds. This finding suggests that private credit grows partly in response to gaps in the financial system, with potentially positive implications for financial stability:

Private credit may be complementing rather than simply competing with banks

It serves borrowers that banks cannot efficiently serve, expanding credit access

Its growth reflects market-driven responses to regulatory changes, suggesting economic efficiency

In terms of economic magnitude, the efficiency of the local banking system has the largest impact on private credit growth, followed by the level of policy rates. This suggests that private credit's expansion is not merely an artifact of the post-2008 low-interest rate environment but reflects more fundamental factors.

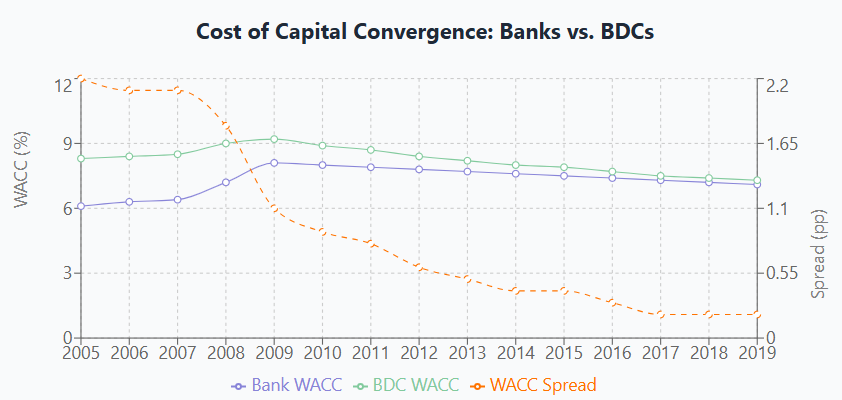

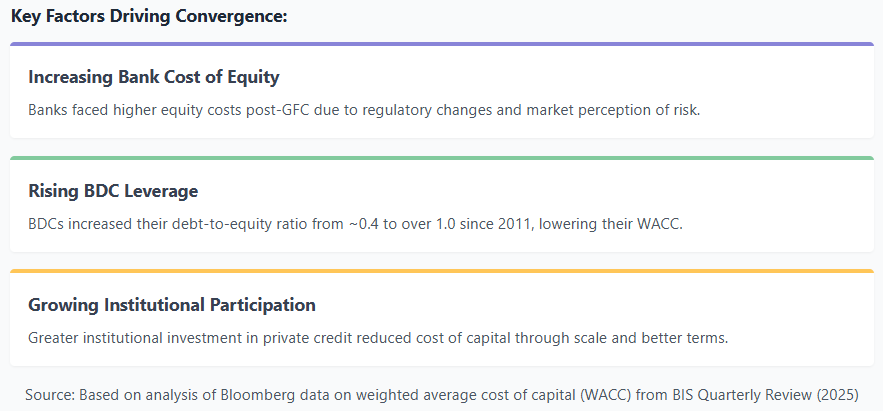

Cost of Capital Convergence: Changing Competitive Dynamics

A fascinating recent development with potential stability implications is the convergence in cost of capital between banks and private credit lenders.

Looking specifically at Business Development Companies (BDCs), an important vehicle for private credit in the US, research shows that the spread between the cost of capital of publicly listed BDCs and that of banks has declined by around 200 basis points between the Global Financial Crisis and 2019.

This convergence stems from two main factors:

A relative increase in banks' cost of equity after the GFC, likely reflecting greater stock market variability due to concerns about bank health

A steady increase in BDC leverage, with their debt-to-equity ratio increasing from around 0.4 to over 1 on average since 2011

These changes have significant stability implications. As the funding advantage of banks erodes, competition between banks and private credit funds intensifies. While this may benefit borrowers through more competitive pricing, it also raises questions about whether private credit's distinctive risk management advantages are being preserved as these lenders take on more bank-like funding structures.

Conclusion: A More Nuanced View of Financial Stability

The rapid growth of private credit represents neither a simple enhancement nor deterioration of financial stability, but rather a complex transformation in how credit risk is distributed throughout the financial system.

Private credit's structural features—particularly the maturity wall—create different incentives compared to bank lending, with implications for both borrower behaviour and system-wide risk. During normal times, these differences likely enhance financial discipline. However, during periods of severe economic stress, they could potentially lead to inefficient liquidations.

As private credit continues to grow and evolve, a few key questions will shape its impact on financial stability:

Will private credit funds maintain their distinctive risk management approach, or will they gradually adopt more bank-like funding structures?

How will regulators balance encouraging innovation and competition while monitoring potential systemic risks?

How will private credit perform during a full economic cycle, particularly during a severe downturn?

What seems clear is that private credit has become a permanent feature of the financial landscape, adding both resilience through diversity and new complexities to monitor. For investors, borrowers, and policymakers alike, understanding these dynamics will be essential for navigating the evolving lending landscape.

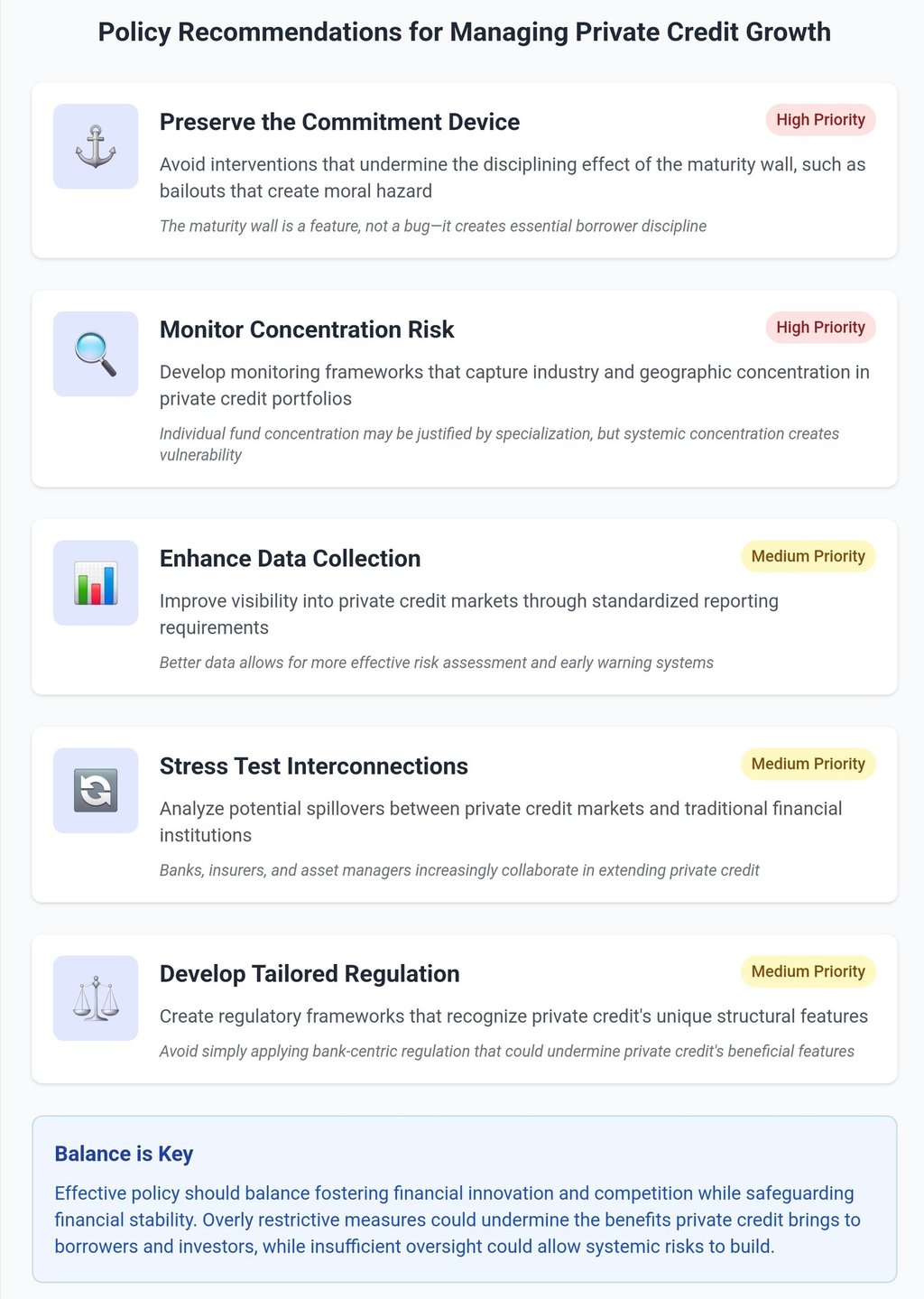

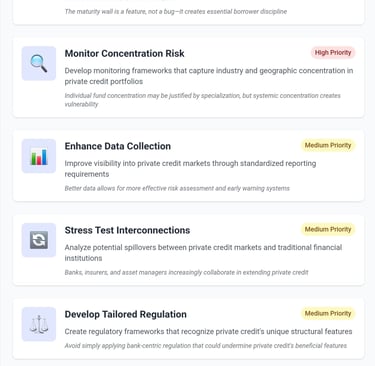

Policy Implications: Balancing Innovation and Stability

The growth of private credit presents both opportunities and challenges for financial stability policy.

Benefits of Structural Diversity

One potentially positive aspect is that private credit could complement the existing bank-based system and bring financial stability benefits. As the BIS notes, "Banks are primarily financed via short-term deposits, and uninsured deposits are prone to runs. Private credit funds, with their closed-end structure and matched maturity of assets and liabilities, may be better positioned to hold long-term loans and attendant risks".

This structural diversity—where different types of financial institutions hold different types of risk—may enhance overall system resilience if properly managed.

Monitoring Concentration Risk

However, regulators should be attentive to concentration risks within private credit portfolios. As noted earlier, private credit funds tend to have highly concentrated portfolios, which may be justified by superior screening and monitoring capabilities but also creates vulnerability to sector-specific shocks.

As private credit continues to grow, systemic risk monitoring should include analysis of potential correlation across seemingly diverse private credit portfolios—particularly during periods of financial stress.

Safeguarding the Commitment Device

Interestingly, the maturity wall that can lead to potentially inefficient liquidation is a feature, not a bug—it's an essential part of private credit's business model as it ensures borrower discipline.

Therefore, policy interventions should avoid undermining this commitment device through ex-post bailouts that could create moral hazard problems. As Albuquerque and Zawadowski caution, "saving borrowers ex post... undermines the ex ante incentives provided via the limited lifetime of private credit funds".

References and Resources

Academic Papers & Research

Albuquerque, R., & Zawadowski, A. (2025). Private Credit: Risks and Benefits of a Maturity Wall. https://www.nber.org/papers/w30868

Boyarchenko, N., & Elias, L. (2024). Financing Private Credit. Federal Reserve Bank of New York Staff Reports. https://www.newyorkfed.org/research/staff_reports/sr1111

Bolton, P., & Scharfstein, D. S. (1990). A Theory of Predation Based on Agency Problems in Financial Contracting. American Economic Review, 80(1), 93-106.

Jang, Y. S. (2024). Are Direct Lenders More Like Banks or Arm's-Length Investors? https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4529656

Industry Reports & Publications

BIS Quarterly Review. (2025). The Global Drivers of Private Credit. https://www.bis.org/publ/qtrpdf/r_qt2503f.htm

International Monetary Fund. (2024). The Rise and Risks of Private Credit. Global Financial Stability Report. https://www.imf.org/en/Publications/GFSR

Alternative Investment Management Association. (2023). Financing the Economy. https://acc.aima.org/research/financing-the-economy.html

Data Sources

PitchBook Data Inc. - Private credit deals database: https://pitchbook.com/data

Preqin Private Debt Database: https://www.preqin.com/data/private-debt

Federal Reserve Financial Accounts of the United States (Z.1): https://www.federalreserve.gov/releases/z1/

S&P LCD Leveraged Loan Data: https://www.spglobal.com/marketintelligence/en/solutions/lcd

Bloomberg Terminal - WACC and cost of capital metrics for banks and BDCs